Planning & budgeting

Saving & investing

KiwiSaver

Tackling debt

Protecting wealth

Retirement

Home buying

Life events

Setting goals

Money tracking

Plan your spending with a budget

Getting advice

Studying

Get better with money

What pūtea beliefs do you have?

How to build up your emergency savings to cover unexpected costs

How to save your money

How to start investing

Find a financial adviser to help you invest

Your investment profile

Compound interest

Net worth

Types of investments

Term deposits

Bonds

Investment funds

Shares

Property investment

How KiwiSaver works and why it's worth joining

How to pick the right KiwiSaver fund

Make the most of KiwiSaver and grow your balance

How KiwiSaver can help you get into your first home

Applying for a KiwiSaver hardship withdrawal

How to use buy now pay later

What you really need to know before you use credit

How to get out of debt quickly

Credit reports

Know your rights

Pros and cons of debt consolidation

Credit cards

Car loans

Personal loans

Hire purchase

Student loans

Getting a fine

What happens if I start to struggle with moni?

How to build up your emergency savings to cover unexpected costs

Cryptocurrency

How to protect yourself from fraud and being scammed

About insurance

Insurance types

Insuring ourselves

Wills

Enduring powers of attorney

Family trusts

Insuring our homes

Losing a partner

Redundancy

Serious diagnosis

How to cope with the aftermath of fraud

Separation

About NZ Super – how much is it?

When you’re thinking of living in a retirement village

How to plan, save and invest for retirement

Manage your money in retirement

Find housing options in retirement

Four approaches to spending in retirement

Planning & budgeting

Saving & investing

KiwiSaver

Tackling debt

Protecting wealth

Retirement

Home buying

Life events

4 October 2021

Reading time: 5 minutes

Posted by Tom Hartmann,

0 comments

When you’re craving one, eating a Big Mac has short-term benefits. Really short term, like feeling full and satisfied in the moment. But what would happen if we invested that money to get some long-term gains?

The price of Macca’s most famous double burger – the one with two patties, special sauce and the extra bun slice in the middle – gets tracked a lot. While it was just US$0.75 in 1967, when it came out, these days it can be found on Uber Eats for all of NZ$8.30.

Okay, so say you took that $8.30 and invested it in shares over 45 years. And just left it there.

We forecast that your return from a managed fund invested in shares, or an aggressive KiwiSaver fund invested in shares, might be 5.5% on average (taking into account fees, taxes, inflation). After 45 years, your $8.30 would grow to $92.

That’s a big return on the price of just one Big Mac! It’s thanks to the power of compounding interest – you earn interest on your money, then that interest earns interest, which earns even more interest, and so on.

Let’s say you invested the price of a Big Mac every week instead. That’s almost $432 a year.

You’d be putting in $19,422 over 45 years, and at the same 5.5% return, you’d come out with $83,836. How about that – your money has quadrupled. That’s what investing little and often does for you.

Up to now we’ve been talking about investing over 45 years, but it’s also intriguing to look at what happens over 20 years. Not just any 20, mind you, but rather how investing over the first 20 years of your working life compares to investing over just the last 20 before age 65.

If you invested the price of Big Mac every week for the first 20 years and then left it alone until age 65, it would multiply by 7. You’d end up with a total of $65,611. You put in $9,064, and the rest would come from returns ($56,547).

But if instead you put off investing your Big Mac money until the last 20 years before age 65 – which many of us do as we enter our highest earning years – the results are less impressive.

You’d end up with just $17,205 – not even double what you put in. You’d invest that same $9,064 but earn just $8,142 in returns.

In both examples you’ve put in $9,064 of your own money, but doing that earlier in life meant a $56,547 return, compared with doing it later and getting a much smaller $8,142 return.

Point being: the earlier we start our investing – even if it’s just the price of a Big Mac – the better off we’ll be in the long term. That’s the power of compounding over time – the longer your money is invested, the better returns you should earn.

Investing is about riding the market’s waves of growth by regularly drip feeding into it (much like we do with KiwiSaver over our working lives).

We typically estimate our future results using an average, much like with the 5.5% return above. But the future will be much more varied, with many more ups and downs. In aggressive funds, for example, our results could range from as high as 22.5% to as low as ‑12.9%.

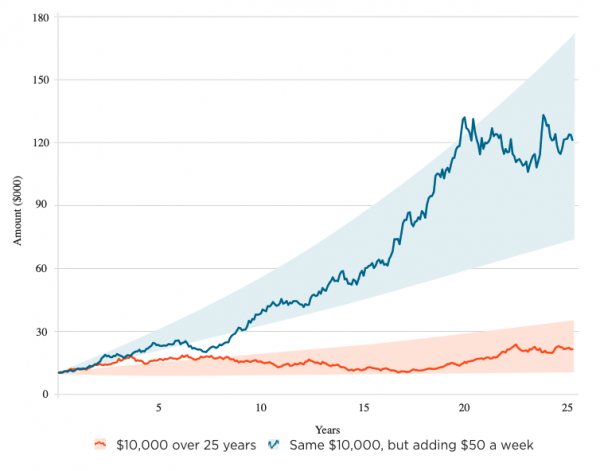

Have a look at these two lines, which are simulations for aggressive funds over 25 years. The lower orange one is if you started with $10,000 and left it invested on its own. The blue one is if you put in that $10,000 and added $50 to it every week.

In orange, if you invested $10,000 over 25 years, there’s only so much you could achieve. In this simulation with a 5.5% annual return your $10,000 would grow to $21,200. (Although you more than double your money, it’s pretty flat, right?)

In the real world, the market goes up and down so you could end up with results somewhere between $10,100 and $34,700 (the orange shaded area).

But above in blue, if you invested $10,000 and added $50 each week, that grows to $131,500. (Much better.) And your range of potential results becomes much wider and climbs much higher – somewhere between $74,200 and $170,900.

By investing regularly, you’re able to take advantage of the possibility of those larger jumps in value when they happen. As they say, you’ve got to be in it…

The other advantage of regularly drip-feeding money into your investments over the years is that you buy gradually, steadily. In many ways this is safer investing. If you dumped all your money in just before a steep fall – like one caused by the pandemic – this could be dangerous.

The big losses could be difficult to stomach, and you might give up on the whole thing before the markets recover. (Happily, they did bounce back quite quickly after COVID-19 hit. Sadly, most who had fled the market missed out.)

Investing a bit at a time sees your money growing, potentially a bit more or a bit less, but over time heading in the right direction.

As you drip feed your money in and buy investments like shares, their price could be low or high at that given time.

When shares are more expensive, for example, you end up buying fewer of them – and when they’re cheaper you buy more. Just what you want, right? Buy less when prices are high, buy more when things are on sale. Genius.

All of this is making me a bit hungry though. As I couldn’t get to a Macca’s in lockdown, it was easier to make something at home and get investing instead.

Visit us on social

© Office of the Retirement Commissioner

Use verification code from your authenticator app. How to use authenticator apps.

Don't have an account? Sign up

Or log in with our social media platforms

A free account gives you your very own space where you can save your tools and track your progress as you get ahead.

Or sign up using Google:

Comments (0)

Comments

No one has commented on this page yet.

RSS feed for comments on this page | RSS feed for all comments