23 September 2019

Reading time: 4 minutes

Posted by Tom Hartmann,

0 comments

Living “sorted” is not just good for your bank balance; it’s good for your mental health, too. The line connecting financial wellbeing with general wellbeing is easy to draw.

To support Mental Health Awareness Week, we surveyed more than 2,600 people. Far too many of us are worried about our finances. It turns out 69% of us are concerned about money, and that affects us in all sorts of ways.

Some of us are feeling the pinch more than others: 74% of women and 82% of those aged 18–34. Māori and Pasifika were also particularly affected – 83% of Māori and 82% of Pasifika were concerned about money, compared to 67% of NZ Europeans. That is so high!

All of this, of course, affects our mindsets and mental wellbeing. And it makes us think and act in a variety of ways. Those surveyed reported that their money concerns made them:

Only 8% sought help to deal with money-related stress. Which is a shame, because there is help available.

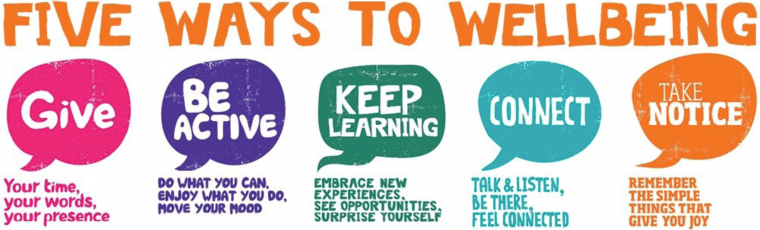

Mental health experts have found five ways to help boost wellbeing. Each of these everyday activities can be done with your money as well.

Talking about money is admittedly challenging, and debt especially brings silence. Yet sharing a problem can be the best way to begin to tackle it. If you’re getting ready to open your own money chat with someone close to you, you’ll find ideas and support here.

It’s easy to get in a funk about your money situation sometimes. But there are active steps you can take to make things better. If you’re looking to sort your finances (and improve your mental wellbeing in the process), here are our six steps to start. Just setting up a safety net will see your anxiety levels come down. Here’s to that!

How much value do we get for our money? Paying more does not necessarily mean we get something of better quality. Can we buy more Christmas by spending more on gifts? Questions like these help us focus on spending money only on things that will improve our wellbeing.

And your money. This is the obvious one – being generous. But we can also “give” our needs when we have them. Putting them on the table means that we open up to connecting with others. Feeling gratitude has been shown to help us make better money choices as well.

For most of us in KiwiSaver, investing our savings is brand new territory to be explored. Where is our money flowing? What investments are we buying? Are they ethical? There is a world of opportunities to look into and make choices about. The more we learn, the more we can get our money working for us, instead of us working for it. And through our decisions, we can better the world in the process. Surprise yourself!

Mental Health Awareness Week is 23–29 September. If you feel you or someone else is at risk or harm right now, phone 111 or see these other options. For free, confidential help with your finances, reach out to the team at MoneyTalks.

Visit us on social

© Office of the Retirement Commissioner

Use verification code from your authenticator app. How to use authenticator apps.

Don't have an account? Sign up

Or log in with our social media platforms

A free account gives you your very own space where you can save your tools and track your progress as you get ahead.

Or sign up using Google:

Comments (0)

Comments

No one has commented on this page yet.

RSS feed for comments on this page | RSS feed for all comments