9 May 2016

Reading time: 3 minutes

Posted by Tom Hartmann,

2 comments

What goes up, must pay out. Just last week a friend was impressed how, after hopping onto the KiwiSaver bandwagon back when it started in 2007, he is now seeing his balance edge past $70,000. With many more years of contributing ahead, he and his family are on track to accumulate more than a modest bit of dosh for their future.

But what happens when they become eligible to withdraw it all? How will they manage hundreds of thousands of dollars in a way that will provide them with regular payments without running out of money? What happens if they want to spend on some big things like a car or trip overseas – does that mean they won’t eat as well in their 80s? It’s complicated.

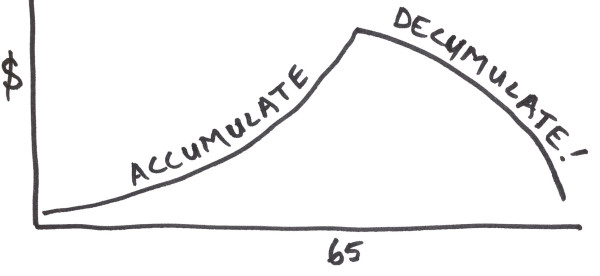

Converting retirement savings to income is being called “decumulation”, but the word hasn’t quite arrived yet; there are no matches on Oxford online, for instance. When it comes to spending the retirement fund, perhaps it could have been “draw-down” or “decrease” – but hopefully not “dispose” or “destroy”!

“Decumulate” really only makes sense if you couple it with its partner, “accumulate” – heaping up funds by investing in schemes like KiwiSaver and then managing those funds in a way to get a steady income in retirement. So not the prettiest of terms, “decumulation”, but fundamentally important to understand when you’re forward thinking.

The stakes are high. When I think about the newly retired, what comes to mind are high-earning sports figures or lottery winners, and many of us will have heard their hard-luck stories of money lost. Just like them, retirees have incredibly important choices to make for their money saved, with slim chance of becoming rich all over again if they make a poor one. There’s no real practice for this, so planning, studying options and getting quality advice become all the more essential.

Sorted’s retirement planner estimates how much of a regular income we can expect when we build up a certain amount. It’s not the nest egg that matters, but what the chicks look like, after all. But the tool does not show anyone how to actually generate income from a lump sum. It takes some savvy investing to do this and not run out of money.

An online poll on these issues is part of this year’s review of retirement income policies. At the time of writing it shows:

Happily, there are some solutions for spinning off a regular income in retirement. For instance, you could arrange with your KiwiSaver provider to draw down your funds gradually, leaving the rest still invested until you need it. For some, releasing the equity of their home through a reverse mortgage may be useful. Also, financial planners can design investment strategies for your nest egg that keep those “chicks” coming regularly.

So these are some ways to tackle the D-word: “decumulation” – which is worth thinking about as we’re “accumulating” savings for retirement. What will be your solution?

Visit us on social

© Office of the Retirement Commissioner

Use verification code from your authenticator app. How to use authenticator apps.

Don't have an account? Sign up

Or log in with our social media platforms

A free account gives you your very own space where you can save your tools and track your progress as you get ahead.

Or sign up using Google:

Comments (2)

Comments

Tom from Sorted | 8 January 26

Thanks for commenting Caryl, and for bringing up those rules of thumb. Since this blog was written we came out with a guide that covers those approaches and more, which you'll find here: https://sorted.org.nz/guides/retirement/four-approaches-to-spending-in-retirement/. Don't miss our new retirement navigator tool above too, which runs scenarios for your spending after you step back from paid work someday...

Caryl | 2 January 26

Good general information but no detailed explanation for the 4% and 6% drawdown rules.

No one has commented on this page yet.

RSS feed for comments on this page | RSS feed for all comments